You know your credit score is important. It affects your ability to get credit cards, loans, mortgages, and even a cell phone plan. When your credit is damaged, how long does the damage last?

What Is A Credit Score?

Your credit score is a three-digit number compiled from many different pieces of information about your credit history. It is based upon how much debt you carry, the amount of available credit, your payment history, the different types of credit you have, the length of your credit history, and how much is new credit. The range of a credit score is 300-850 with 300 being the lowest and 850 being perfect. Once you have missed a payment on an account or become delinquent, the creditor will report this to the credit reporting agencies. The credit score is used by potential lenders to determine your creditworthiness. The higher your score, the more likely you are to be approved for financing or credit accounts. It will also potentially affect the interest rate you receive. In essence, lenders look at your credit score as a measure of the risk they will undertake in loaning you money.

The Life Cycle Of Your Debt

When you carry debt, whether in the form of a credit card, a mortgage, a student loan, or a car note, the creditor makes a report to the three national credit reporting agencies: Experian, EquiFax, and TransUnion. Your creditor will report both good and bad information. Your creditor may report to the credit reporting agencies on a daily or monthly basis, or even less frequently. Therefore, changes to your credit score as a result of bad information may not show up right away. That is why it is a great idea to check your credit report and credit score regularly to ensure that the information provided therein is accurate and to confirm that there is no erroneous information of evidence of identity theft.

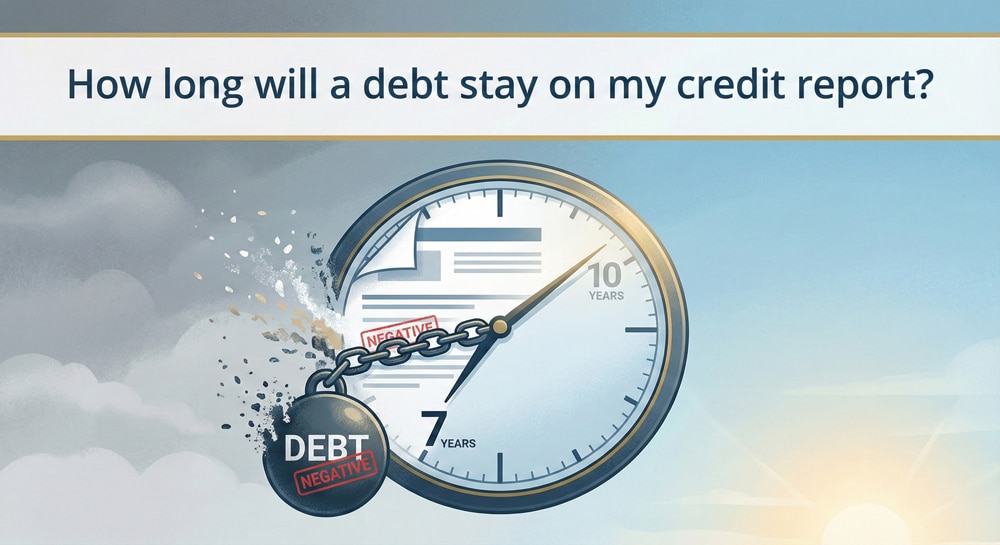

Most negative items can generally be reported for up to seven years, while bankruptcy can remain for up to 10 years under federal law. In practice, the nationwide bureaus typically remove Chapter 13 bankruptcies about seven years from the filing date and Chapter 7 about ten years from the filing date. California also has some exceptions with regard to tax liens and how long they will remain on your credit report. Paid or “released” tax liens will remain on your report for 7 years from the date of release or 10 years from the date it was filed while unpaid or “unreleased” tax liens remain on your report for 10 years from the filing date. Positive credit information can remain a part of your credit history for the rest of your life.

California: Statute Of Limitations On Debt

The length of time negative information remains on your credit report should not be confused with the statute of limitations for that debt. The statute of limitations is the amount of time that the creditor has to pursue legal action against the debtor for the debt. There are different statutes of limitations in California for different types of debt. The chart below gives a breakdown of the statutes of limitations for the most common debts:

| Written Contract | Oral Contract | Promissory Note | Open-ended accounts (including credit cards) |

| 4 years | 2 years | 4 years | 4 years |

Just because the statute of limitations has run on a debt does NOT mean that it will automatically cease to negatively affect your credit history. In fact, it does not even mean the creditor will not attempt to collect the debt. Keep records and make sure you that if you receive a debt collection notice or a notice of a lawsuit to collect the debt, the statute of limitations has not expired. If it has expired, you can assert that in court. Then you won’t be liable for the debt. You do, however, have to go to court. The claim won’t automatically be barred by the statute of limitations.

How To Eliminate Debt From Your Credit Report

If you have had negative information reported and want to improve your score, there are some steps you can take to shorten the “life of the debt” as it applies to your credit history. First and foremost, you can satisfy the debt. If you cannot satisfy the debt, you can contact the credit reporting agencies and send them each a 100-word written statement setting out the reason for the occurrence that negatively affected your credit or disputing it. Experian and TransUnion will even allow you to make multiple statements to your report. However, Equifax will only allow one 100-word statement. But use the statement cautiously because it has the potential to hurt rather than help if not worded carefully. For example, if you were in a car accident and became delinquent on certain bills due to your incapacity, you may want to advise of your situation and that you are now fully recovered and satisfying your accounts. Conversely, you would not want to submit a 100-word written statement arguing that the debt was overlooked because you had too many other bills to pay at that time. Always remember that as you begin to repair your credit, the negative marks on your report will stand out less and less to lenders.

How can you manage your credit?

Be proactive. You can check your credit reports for free every week from each of the three major credit bureaus. Regular checks help you spot identity theft, reporting errors, or accounts that should have aged off.Keep track of your credit report and credit score before it begins to drop. Make a debt management plan that fits your budget and begin by ensuring you make all payments on time and attempt to pay more than the minimum payment. If your score is already low, monitor it for improvement as you begin to make positive changes with your debt management plan. Each month, as you stay current and bring your debt down, you should see your score increase. As each month passes, by taking these steps, you will move further away from the negative marks that have brought your score down and you will replace it with good information, moving you closer to an excellent credit score.

If you suspect that a debt collector or lender has reported something incorrectly or participated in illegal debt collection activities, you can contact the Consumer Financial Protection Bureau (CFPB). The CFPB is a federal watchdog that regulates the actions of debt collectors while protecting consumers. You can also consult with an attorney who specializes in defending consumers against debt collection to ensure your rights have not been violated.

If you’re struggling with debt, we may be able to help. Contact us today for a free consultation with one of our experienced California bankruptcy attorneys. We can help you evaluate your options for debt management and choose the right strategy for your needs, whether it’s consolidation, bankruptcy, or other methods.